The General Policy Declaration of the new head of the Senegalese government is expected within days or weeks to come. The question of the budget will undoubtedly be one of the important subjects which will be addressed by Prime Minister Mr. Ousmane Sonko during his address to the National Representation. He is, in fact, a crucial subject which concerns all citizens, because it relates to the way in which our Money, for all of us, is managed by administrative authorities.

However, the texts of finance laws which define the Nation's budget are of such complexity that only public finance specialists or those who take the trouble to understand them study seriously, this is our case, are able to grasp all the aspects. This is all the more more regrettable than this ignorance of budget mechanisms and their implications in life national is a breeding ground for bad governance, which leads our governments to do a little anything with our financial resources without being challenged by their constituents that we are.

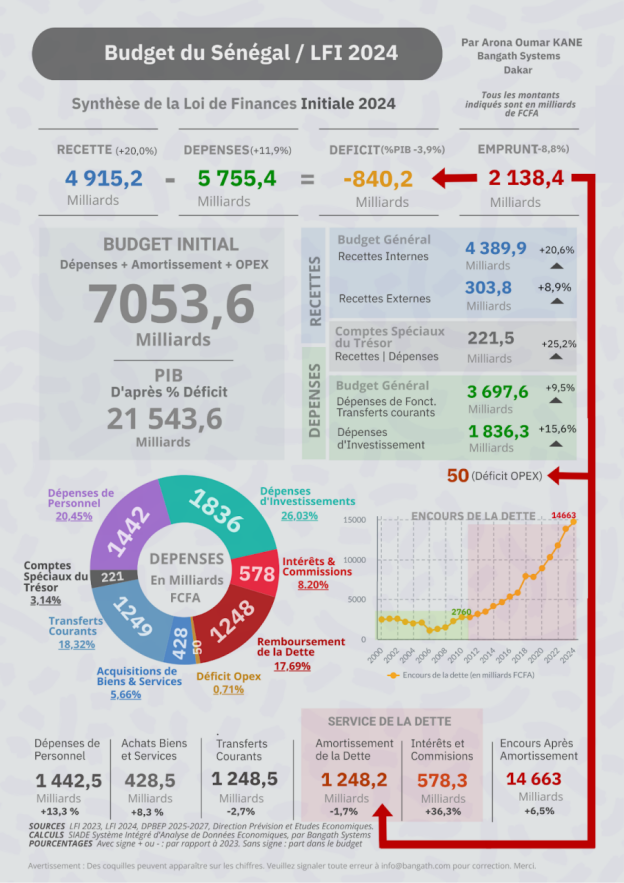

To help the average citizen have a better understanding of the budget and break this logic of widespread ignorance of budget management, we have designed a model for summarizing the text of finance law. This synthesis should allow, thanks to simple graphics and diagrams on a single page and a glossary, to grasp the salient points and to understand the meaning of the main aggregates of the finance law, their interconnections and their implications.

The objective pursued in this article, and those that we regularly publish, is to allow a better citizen monitoring on the governance of our resources and to inform public debate on little-known aspects of budget management. This will, in this case, avoid manipulation, in particular of those who already compare the budgetary management of the new authorities with their own when they were in power. The new government is in reality, so far, only executing the Budget which they inherited, which is also regrettable. A amending finance law should have been presented above all else, in view of the scandalous imbalance which continues to exist between expenditure operating and those devoted to investment. We hope that with this summary graphic, these issues will be better understood by our fellow citizens.

Explanatory Notes

Finance Law

The finance law is a law adopted by parliament which determines, for a calendar year, the nature, amount and allocation of State resources and charges (receipts and expenses). It is the main instrument of state budgetary and tax policy.

Amending Finance Law

A amending finance law modifies, during the year, the provisions of the finance law initial. It makes it possible to adjust revenue and expenditure forecasts according to developments unforeseen economic and financial consequences.

General Budget

The general budget of Senegal represents all the resources and expenses of the State for a given budget year. It includes all revenue collected and expenditure made by the government in the context of its economic and social functions.

Treasury Special Accounts

Treasury special accounts are specific accounts managed by the state outside the budget general. They are used for specific financial transactions that require separate accounting. They balance each other in revenue and expenditure.

Initial Budget

The initial budget corresponds to the amount set in the initial finance law. Its amount is equal to the expected revenues, increased by the borrowing envisaged for the year. In principle, the loan is not supposed to be taken into account in the Budget, but this summary reflects the figures validated by the Initial Finance Law 2024. The other particularity of this 2024 budget is that it succeeds a other initial budget without an amending finance law between the two, despite the big differences between the achievements at the end of 2023 and the forecasts of the initial finance law. A responsibility jointly of the outgoing government, the National Assembly and the Court of Auditors, and a a failure which says a lot about the seriousness and rigor put into the keeping of our public accounts.

Recipes

Revenue represents all financial resources collected by the State. They divide into two main categories: internal revenues and external revenues.

Internal Recipes

Internal revenue comes from resources generated within the country, including taxes, taxes, customs duties, royalties and social security contributions. They are crucial for the financing of public expenditure without depending on the outside.

External Recipes

External revenues are financial resources obtained from outside the country. They include financial aid, donations obtained from international institutions or countries foreigners. Not to be confused with borrowing which fuels debt.

Expenses

Expenditure includes all government disbursements to finance its activities and programs. They are subdivided into several categories, including operating expenses and investment expenses, interest and debt fees.

Deficit

The budget deficit occurs when government expenditure exceeds its revenue. It indicates a need for additional financing that the government must meet, often through borrowing. When expenditures are less than revenues, we speak of a surplus.

Loan

Borrowing is a source of financing for the State when there is a budget deficit. The government borrows funds from domestic and international financial markets to cover its financing needs. This is how a Eurobond issue was carried out to cover a part of the loan provided for in the 2024 finance law, set at 2,138.4 billion FCFA. Our synthesis clearly shows that this loan, supplemented among other things by the Special Drawing Rights of the IMF with the conditions that we know, serves much more to repay other debts than to finance the deficit and therefore the investments which should have been the exclusive receptacle of the debt.

Depreciation

Amortization represents an amount paid to government creditors to reduce the outstanding debt. debt. In principle, depreciation should be done with the growth generated, thanks to revenues internal. But when the debt contracted is not used wisely to fund productive investment but exposed to mismanagement and diversion of objectives, combined with the absence of evaluation of its real impact on growth, it will only serve to play the pomps funerals for hyenas - suul bukki sulli bukki, the Senegalese understand.

Debt Interest

Debt interest is the periodic payment made by the State to remunerate the lenders. They constitute a financial burden linked to loans. They are included in the expenses general budget or operating expenses.

Debt Commissions

Debt fees are additional fees associated with management and underwriting loans. They include advisory fees, warranty fees, and other financial costs. These commissions, often drowned out by abuse of language in the names "financial charges of the debt" with the interest on the debt, are increasingly higher because the interest and commissions combined even exceed the principal repaid in certain months, with amounts that could not be only explain the interest rates announced. It would be useful if the government or a commission parliamentary inquiry looks into these commissions to find out their exact structure and the beneficiaries. We cannot continue to pay hundreds of billions of FCFA in commissions without know exactly to whom, in what capacity and whether the service provided is worthy of this exorbitant cost.

Debt Service

Debt service includes all payments made to honor loans, including depreciation, interest and commissions. It is a significant part of state spending.

Personnel Expenses

Personnel costs relate to salaries and wages paid to civilian servants and state employees. They constitute a significant part of operating expenses.

Purchases of Goods and Services

These purchases cover expenses related to the acquisition of goods and services necessary for functioning of public administrations, such as cars, real estate, travel, organization of events.

Current Transfers

Current transfers include subsidies, allocations to constitutional institutions, to public companies and local authorities, social assistance and others transfer payments made by the State without direct compensation.

Operating Expenses

Operating expenses, or ordinary expenses, include all the necessary costs the day-to-day operation of public services. They include salaries, purchases of goods and services, current transfers and the financial burden of debt.

Investment Expenditures

Investment expenditures, or capital expenditures, relate to funds used to finance long-term projects, such as infrastructure, public facilities, and programs of development. They aim to improve the productive capacity of the country.

Sources

- Law 2022-22 of December 9, 2022 relating to the finance law for the year 2023

- Law 2023-18 of December 15, 2023 relating to the finance law for the year 2024

- Dashboards of the Senegalese Economy by the DPEE

- Calculations and Analysis with SIADE, Integrated Economic Data Analysis System by Bangath Systems

- Multi-year Budgetary and Economic Programming Document 2025-2027